20240830145908.gif)

The McKinsey and Business of Fashion Report on State of Fashion argues that the industry is in a flux. Technology, innovation, digitalisation, transparency, fashion immediacy, restructuring of supply chains and internal operations are the trends driving industry, writes Anjuli Gopalakrishna

"Uncertain, Changing and Challenging" were the top three words that executives used to describe the state of the fashion industry in 2016 in the recent survey conducted jointly by McKinsey and Business of Fashion. This is not surprising. We have seen multiple sources of turbulence in the recent past: the Brexit vote in the UK, terrorist attacks in various parts of the world, the US election campaign, the slowdown of the Chinese economy, overall volatility of the stock market, digital disruptions in various forms, rapidly evolving consumer expectations and behavior in the wake of technology advancements. These put together have resulted in tremendous pressures on the fashion industry.

The year 2016 experienced the worst sales growth rate of 2-3 per cent with stagnating profit margins. This is in stark contrast to the fashion industry's performance in the previous decade of 2005-2015, which saw the industry grow at a 5.5 per cent annual rate, according to the McKinsey Global Fashion Index. The fashion industry interestingly still remains one of the key global value-creating industries in the world, with a staggering $2.4 trillion in total value. If it were ranked alongside individual countries' GDP, the global fashion industry would represent the world's seventh largest economy.

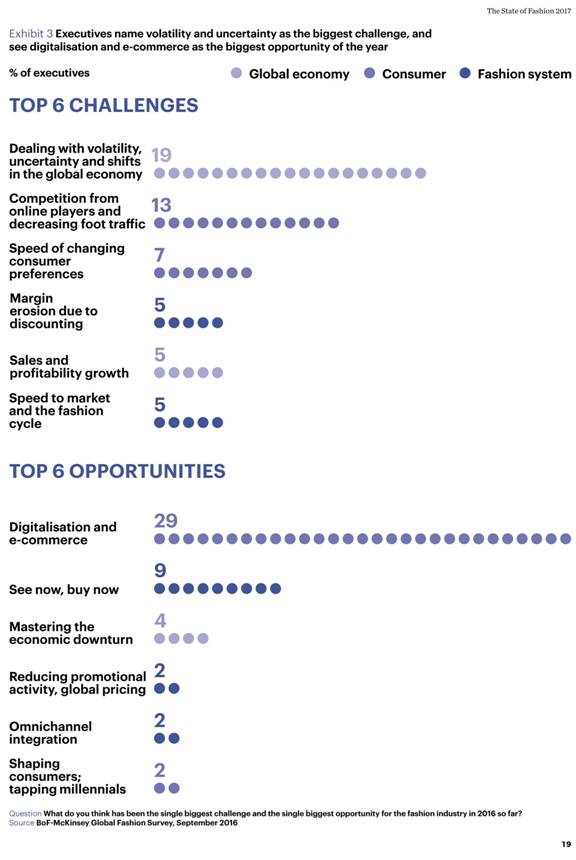

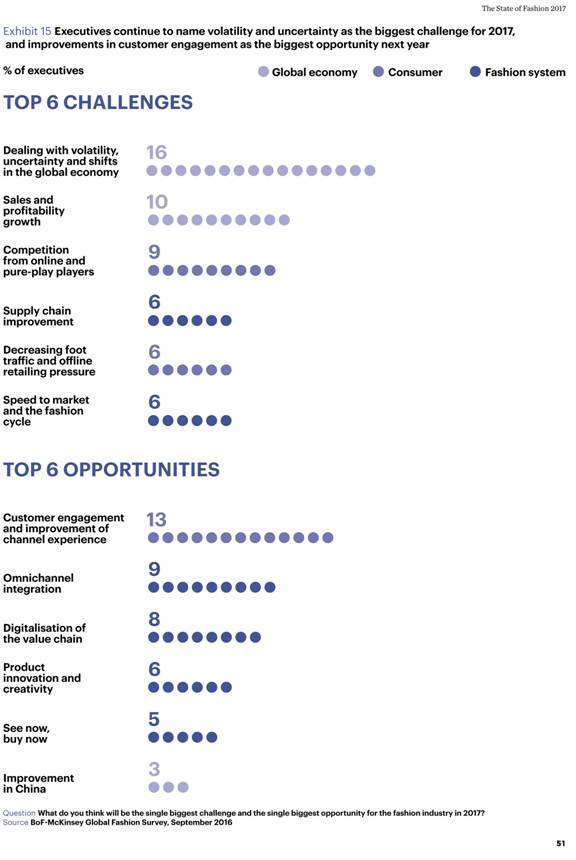

The top challenges and opportunities: 2016 vs 2017

What are the top-of-the-mind issues industry professionals are grappling with? Here is a quick snapshot of the top challenges and opportunities that the survey brought out for 2016 and 2017. Dealing with volatility and uncertainty is certain and here to stay. So are the changing consumer expectations driven by the digital and technological revolution. Today's forever connected, well informed, discerning, customers with shifting loyalties to brands, seeking alignment of their purchases with their deeper values are that much more difficult to please and that much more unpredictable.

Amidst the challenges, we saw some opportunities emerge as well. Top-end players like Burberry, Tom Ford and Tommy Hilfiger successfully launched 'see now, buy now' runway shows to cater to the customer's need for instant gratification. The reconfiguration of the entire design and product development cycle to enable the runway pieces to be made available instantly to end-customers across multiple locations and platforms is an entirely new concept. Whether this will be adopted on a wider scale and in a profitably sustainable way remains to be seen.

What is clear is that brands can no longer afford to ignore changing customer expectations. Only those who pay heed and listen seriously to offer better experiences to their customers will stay in the game. Whether it is in providing instant gratification or providing an overall ease of shopping convenience seamlessly across different channels via omnichannel integration, or in addressing the need for transparency and information via sustainability measures or digitisation of supply chain initiatives are the developments to watch out for. The fashion industry is ripe for disruption and change.

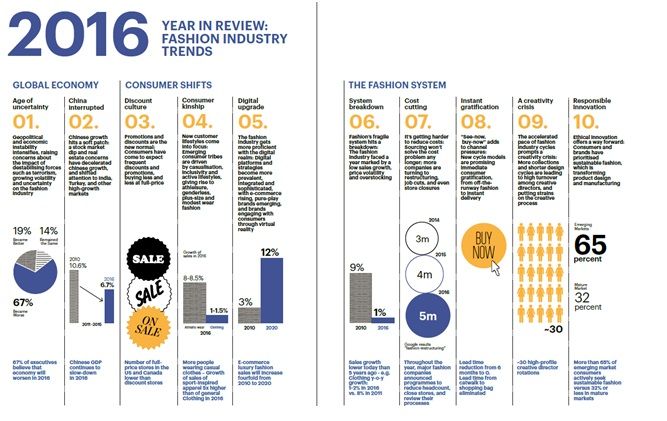

The top trends that will shape fashion industry 2016-2017

Here is a quick snapshot of the key trends that are important from 2016 through 2017, and are likely to influence the direction that fashion players will take.

Notable trends to watch are the global disruptions caused by conflicts, terrorism and financial crises that impact customer sentiment. This is particularly true for the fashion industry as purchase decisions are emotional ones, and if customers feel uncertain or scared, they are less likely to buy.

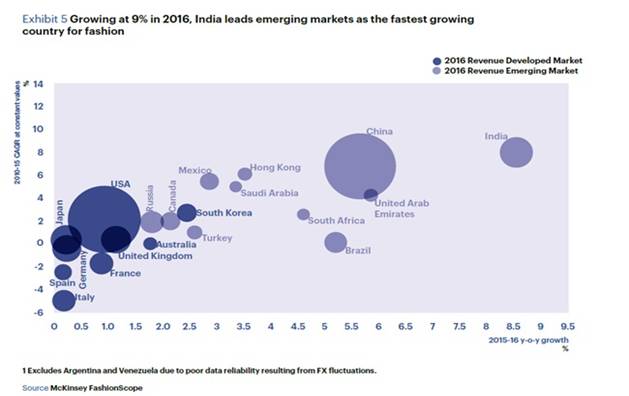

The economic slowdown of China was a major topic of discussion. China's GDP has dropped to 6.7 per cent in 2016 as compared to 7 per cent in 2015. Chinese consumers are becoming more selective about spending, and are allocating more wallet share to services and experiences, and thus moving up the value chain from mass products to premium products. The China market remains an important one due to its sheer size. However, due to the slowdown in sales growth, emerging markets are getting more attention. The highest growth countries predicted are India and the United Arab Emirates. They lag in terms of market size when compared to China and United States. See exhibit below.

Another interesting trend worth talking about is about brands catering to specific consumer lifestyles. Athleticwear and athleisure in response to the casualisation in fashion preferences has become an important trend to watch out for. Genderless fashion emerged for those who are not willing to conform to traditional male-female thinking. Zara launched its first genderless collection in March 2016.

An important category that gained eminence is 'modest-fashion' catering to the needs of Muslims of the Middle East, Southeast Asia and the rest of the world. Dolce and Gabbana, Uniqlo, DKNY, Mango, Tommy Hilfiger and many more global brands are in the game to service this market segment which is likely to be valued at $327 billion based on Global Islamic Economy Report.

International brands are also seeking newer ways to enhance the experience for online and connected shoppers. The latest trend to talk about is the use of virtual reality (VR) by fashion brands to create an immersive experience for consumers. Thirteen shows from the New York Fashion Week were broadcast in 360-degree VR including collections from Prabal Gurung, Rebecca Minkoff. Tommy Hilfiger, Dior and Topshop used VR in their stores to transport shoppers to pre-recorded catwalk shows. While still in a nascent stage, this holds immense promise for creating a differentiated experience for brands. This in addition to the augmented reality (AR) in the form of smart-fitting rooms and mirrors enabled by RFID and AR technology that are redefining consumer experience and expectations in fashion retail.

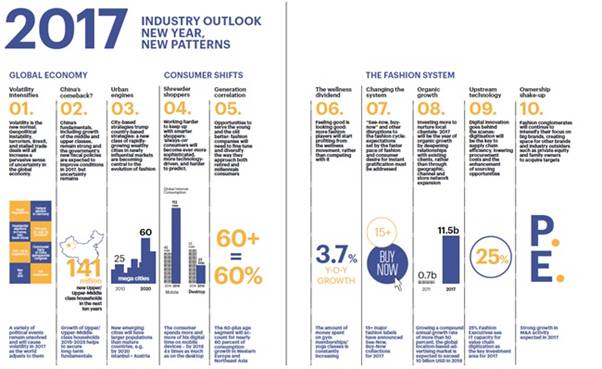

The outlook for 2017 is slightly more optimistic if the McKinsey Global Fashion Index is to be believed. It predicts a growth for fashion industry in the range of 2.5-3.5 per cent for 2017 up from 2.0-2.5 per cent in 2016. The likely winners are in the affordable luxury and value segments.

The most important developments likely to determine the direction for fashion industry are as follows.

Cities as against the countries or regions will be the engines for growth for brands' market expansion and growth strategies. Different segments will have different cities as top markets. For example, Tokyo is likely to be the top market for clothing in 2025, but Hong Kong is likely to ace the list for jewellery, bags and luggage categories. While Los Angeles, Tokyo and New York will be among top 10 largest fashion markets in 2025, emerging cities include Beijing, Mumbai and Shanghai.

The better informed, forever connected, more value conscious and more demanding consumers will put pressure on brands to provide better experience in terms of convenience, price, personalisation and transparency. CRM will be crucial to invest in for any brand serious about staying in the game.

While there is a lot of talk about millennials, the McKinsey survey suggests a sizable market share growth for retired and elderly populations. By 2025, the global population aged over 60 should reach 30 per cent in advanced economies and 13 per cent in emerging economies. Brands would do well to cater to the needs of not just the millennials but this population segment as well.

The race in cost-cutting via sourcing and squeezing suppliers is over. There is no more room for chasing low-cost countries to save costs. The only way forward for fashion companies will be to find operational efficiencies within the fashion system, building transparency and integration in the supply chain with key strategic partners in a collaborative fashion as opposed to traditional buyer-supplier relationships. Technology advancement and digitalisation of supply chain will see significant interest from brands. Adidas' Speed Factory or Nike's Distribution Centre in Belgium designed around sustainable supply chains are steps in the right direction. More companies will focus on organic growth and internal focus towards improving systems, operations and efficiencies, rather an inorganic growth via expansion and acquisitions.

The fashion industry is ready for a shake-up from within. We will see winners and losers emerge depending on who will adapt to the changing game and who will stay stuck in the old way of doing things. Technology, innovation, digitalisation, transparency, fashion immediacy, restructuring of supply chains and internal operations will be the top-of-mind themes to stay, survive and thrive in the new era.

Comments